The budget 2008 has been announced today. The following is the highlights:

- Tax exempt saving fund, up to $5,000 annually. No tax on gain, withdraw anytime without penalty.

- 10.2 Billion to pay down debt.

- Maximum RESP time limit extended to 35 years; contribution period extended by 10 years.

- tax break on capital equipment depreciation extended to 2012

- $500-million for investment in public transit.

- A $2-billion fund for infrastructure investment will be made permanent.

- $250-million over five years to help the automotive industry develop more environmentally friendly vehicles.

- $350-million for a Canada Student Grant Program.

- $90-million for older workers hurt by factory closures.

- $300-million to for nuclear energy.

- $330-million over two years to improve access to safe drinking water for First Nations.

- $400-million to encourage provinces to recruit 2,500 police officers.

- $43 million to Communications Security Establishment

- $75 million to Canada Border Services

- Permanent annual increase in military spending of 2% by 2011

- New organization to administrate EI premium.

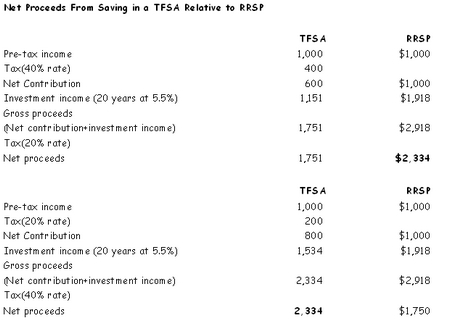

As you might have noticed, there is a new account type being introduced today. It is called Tax Free Saving Account(TFSA).

What is TFSA?

It stands for Tax Free Saving Account. According to the budge 2008, Starting in 2009, people 18 and older will be able to put up to $5,000 per year in a Tax-Free Savings Account and rack up investment gains without paying taxes at any time, including withdrawal. Any unused contribution room will be carried forward just like your RRSP room. The $5,000 annual contribution limit will be indexed to inflation in $500 increments. Contributions to a spouse's or common-law partner's TFSA will be allowed, and TFSA assets will be transferable to the TFSA of a spouse or common-law partner upon death

What is the benefit of TFSA?

The major benefit of TFSA is that it allows the money you put into it to grow tax free.

Don't we have RRSP to allow my money grow tax free already? What is the difference between them?

The differences are:

- Although the money in RRSP can be withdrawn anytime before actual retirement, you are subject to withholding tax while doing it; the money in TFSA could be withdrawn anytime without any withholding tax with all the gains being tax exempt.

- When you withdraw your money from your RRSP account, your contribution room is forever lost. Withdrawals from TFSA will create contribution room for future savings.

- The money put into RRSP is tax deductible. In other words, you get tax refund from contribution in RRSP. The money you put into TFSA is not tax deductible. Therefore, you use after-tax dollar to fund your TFSA account.

What could be held inside TFSA?

You can hold many investment vehicles inside your TFSA, such as stocks, bonds, GIC, mutual funds, etc. However, please note that since all the capital gains inside TFSA is tax free, it also means any capital loss inside it cannot be claimed to be offset your other capital gains or carried forward. So please think carefully before holding any stocks inside TFSA. Technically, TFSA works the best for the fixed income investment vehicles, such as GIC and bonds.

What works the best to be held inside TFSA?

Like I just said, it works the best for fixed income investments. However, if you think you are a very good trader, you can try to trade stocks inside TFSA. If you make 10% profit, all 10% will be tax free. Also, I am thinking it might be good to hold some nice US DIVIDEND stocks such as Bank of America. Since under regular non-registered account, any dividend from US Stock will be considered as income and is taxed at the full tax rate. I think it will be beneficial to hold those inside TFSA.

It will be another year from the date we can actually contribute to TFSA. I think it will be an interesting topic in the personal finance blog world.